Providing health benefits is one of the biggest challenges for small businesses. Many small employers want to support their employees with healthcare coverage, but traditional group health insurance plans can be expensive and difficult to manage. Premiums for group plans often increase every year, and the administrative work involved can be complex for small teams with limited resources.

To solve this problem, the U.S. government introduced a health benefit option designed specifically for smaller companies. One such solution is the Qualified Small Employer Health Reimbursement Arrangement, commonly known as QSEHRA. This program allows small employers to reimburse employees for healthcare expenses instead of purchasing a traditional group health insurance plan.

This guide explains what QSEHRA is, how it works, who qualifies for it, and why it can be a useful option for small businesses looking to provide health benefits in a more flexible and cost-effective way.

What Is QSEHRA?

A Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) is a type of employer-funded health reimbursement benefit that allows small businesses to reimburse employees for medical expenses and health insurance premiums.

QSEHRA was created through the 21st Century Cures Act, which became law in 2016. Before this law was passed, small employers were not allowed to reimburse employees for individual health insurance without facing penalties under federal healthcare regulations. The law introduced QSEHRA to provide a compliant way for small businesses to help employees pay for healthcare.

Under a QSEHRA plan, the employer sets a fixed allowance amount that employees can use for qualified healthcare expenses. Instead of offering a group insurance policy, employees buy their own individual health insurance plans and then receive reimbursement from the employer for eligible costs.

The key purpose of QSEHRA is to give small employers a simpler and more affordable way to offer health benefits without needing to manage a traditional insurance plan.

How QSEHRA Works

QSEHRA works as a reimbursement-based benefit instead of a traditional insurance plan. The employer does not purchase health insurance for employees. Instead, employees buy their own individual health insurance coverage and submit proof of eligible expenses for reimbursement.

Employers decide how much money they want to provide each employee through a monthly or annual allowance. Employees can then use this allowance to cover approved healthcare costs.

Step-by-Step Process

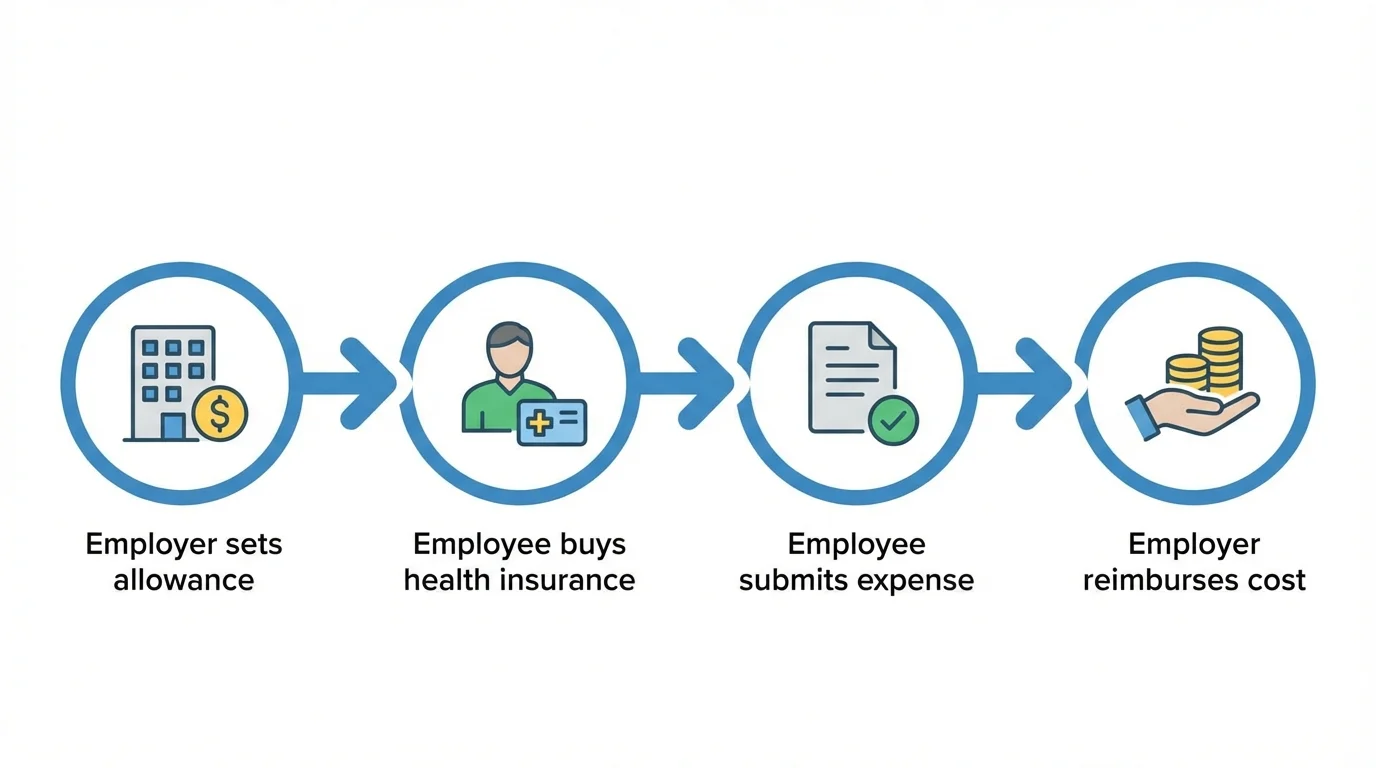

- Employer sets a monthly allowance: The employer determines how much reimbursement money will be available for employees. The allowance amount can vary based on whether the employee has individual coverage or family coverage.

- Employees purchase individual health insurance: Employees choose their own health insurance plan. This can be purchased through the health insurance marketplace or from private insurers.

- Employees submit proof of expenses: When employees pay for healthcare expenses or insurance premiums, they submit documentation showing the cost and that the expense qualifies under IRS rules.

- Employer reimburses approved expenses tax-free: After reviewing the claim, the employer reimburses the employee up to the available allowance. These reimbursements are generally tax-free for the employee if they have qualifying health coverage.

Who Is Eligible for QSEHRA?

Employer Eligibility

Not every business can offer a QSEHRA. The benefit is specifically designed for smaller employers.

- Businesses must have fewer than 50 full-time employees: Organizations that meet this requirement are considered small employers under federal healthcare regulations.

- Employers cannot offer group health insurance: A company cannot offer a QSEHRA if it already provides a group health insurance plan to employees.

- Employers must fund the arrangement: The reimbursement allowance must be paid entirely by the employer. Employees are not allowed to contribute money to the QSEHRA plan.

Employee Eligibility

Most employees within an eligible company can participate in QSEHRA, but employers can apply certain rules.

- Full-time employees typically qualify for the benefit

- Employers may choose to include part-time employees depending on company policy

- Seasonal employees may be excluded in some cases

- Employers may set a waiting period before employees become eligible

Some individuals may not qualify depending on their employment status.

- Independent contractors are generally not eligible

- Certain non-resident employees may be excluded under plan rules

QSEHRA Contribution Limits

The Internal Revenue Service (IRS) sets maximum limits on how much employers can reimburse employees through a QSEHRA each year. These limits are adjusted periodically to account for inflation.

Employers cannot exceed the annual reimbursement cap established by the IRS. However, they can offer any amount below that limit.

The contribution limits differ depending on the employee’s coverage type.

- One limit applies to employees with individual health coverage

- A higher limit applies to employees with family coverage

Employers typically divide the annual limit into monthly allowances that employees can claim throughout the year.

The flexibility within these limits allows businesses to choose reimbursement amounts that match their budget while still offering meaningful health benefits.

Expenses Covered Under QSEHRA

QSEHRA can reimburse a wide range of healthcare expenses that are considered qualified medical costs under IRS guidelines.

Health Insurance Premiums

Employees can use their QSEHRA allowance to reimburse the cost of health insurance premiums.

- Individual health insurance plans purchased through government marketplaces

- Health insurance policies purchased directly from private insurers

Qualified Medical Expenses

QSEHRA can also cover many out-of-pocket healthcare costs if they qualify under federal tax rules.

- Doctor visits and medical consultations

- Prescription medications

- Preventive care services

- Dental treatments

- Vision care such as eye exams or glasses

- Other medical expenses defined as eligible under IRS healthcare expense rules

Employees must provide documentation to prove that these expenses qualify before reimbursement can be approved.

Tax Benefits of QSEHRA

Benefits for Employers

Employers receive several tax advantages when offering QSEHRA.

- Reimbursements are considered tax-deductible business expenses

- Employers generally do not pay payroll taxes on reimbursements made through the plan

These tax benefits can make QSEHRA more cost-effective compared to traditional health insurance benefits.

Benefits for Employees

Employees also benefit from favorable tax treatment.

- Reimbursements received through QSEHRA are generally tax-free

- Employees can reduce their personal healthcare costs with employer support

To receive tax-free reimbursements, employees must maintain minimum essential health coverage as required under federal healthcare regulations.

Advantages of QSEHRA for Small Businesses

QSEHRA offers several advantages that make it attractive for small employers.

- Lower overall healthcare costs compared to many group insurance plans

- Predictable budgeting since employers control the allowance amount

- Flexibility for employees to choose their own insurance plans

- Reduced administrative work compared to managing a full insurance policy

- Ability to offer health benefits even with a small workforce

These advantages allow small businesses to provide healthcare support while maintaining financial control.

Limitations of QSEHRA

Despite its advantages, QSEHRA also has certain limitations that employers should consider.

- The benefit is only available to employers with fewer than 50 full-time employees

- Companies offering group health insurance cannot provide QSEHRA at the same time

- Annual reimbursement limits are set by the IRS

- Employers must follow specific documentation and compliance requirements

- Employees must have qualifying health coverage to receive tax-free reimbursements

Understanding these limitations helps employers decide whether QSEHRA is the right option for their organization.

QSEHRA vs Traditional Group Health Insurance

Key Differences

QSEHRA and traditional group health insurance operate in very different ways.

- Group health insurance involves purchasing a single insurance plan that covers all employees

- QSEHRA provides reimbursement for healthcare expenses instead of offering a group plan

- Group plans typically have fixed coverage options chosen by the employer

- QSEHRA allows employees to select their own insurance plans based on personal needs

- Administrative responsibilities differ, with group plans often requiring more management

When QSEHRA Is a Better Option

QSEHRA can be a better option for certain types of businesses.

- Small businesses with limited healthcare budgets

- Companies with remote employees who may need different insurance plans

- Employers who want predictable healthcare costs without managing a group policy

In these situations, the flexibility of QSEHRA may be more practical than a traditional insurance plan.

QSEHRA vs ICHRA

What Is ICHRA?

An Individual Coverage Health Reimbursement Arrangement (ICHRA) is another type of employer-funded reimbursement program that allows employers to reimburse employees for individual health insurance and medical expenses.

Unlike QSEHRA, ICHRA can be offered by businesses of any size, including large employers.

Major Differences Between QSEHRA and ICHRA

- QSEHRA is limited to small employers with fewer than 50 full-time employees

- ICHRA can be offered by employers of any size

- QSEHRA has annual contribution limits set by the IRS

- ICHRA does not have the same federal reimbursement caps

- ICHRA allows employers to create different employee classes with different benefits

- QSEHRA typically applies to all eligible employees within the company

Understanding these differences helps employers select the most appropriate reimbursement arrangement.

How to Set Up a QSEHRA

Step 1: Determine Eligibility

The first step is confirming that the business qualifies as a small employer under federal healthcare rules and does not currently offer group health insurance.

Step 2: Decide Contribution Amount

Employers must choose how much money they want to offer employees as reimbursement allowances within the limits set by the IRS.

Step 3: Create Plan Documents

Employers must prepare official plan documents outlining how the QSEHRA program works, including eligibility rules, reimbursement limits, and procedures.

Step 4: Notify Employees

Employers must provide written notice to eligible employees explaining the details of the QSEHRA benefit before the plan begins.

Step 5: Manage Reimbursements

Employers must review submitted healthcare expense claims and reimburse approved expenses according to the plan rules.

Compliance and Legal Requirements

QSEHRA plans must follow several regulatory requirements to remain compliant with federal law.

- Employers must provide a written notice to employees explaining the QSEHRA benefit

- Documentation of eligible expenses must be maintained for reimbursement records

- Employers must follow IRS reporting requirements related to QSEHRA benefits

- Personal medical information must be handled according to privacy and security standards

Maintaining proper documentation and following these rules helps prevent compliance issues.

Best Practices for Managing QSEHRA

Proper management ensures that a QSEHRA program runs smoothly.

- Set reimbursement allowances that align with business budgets and employee needs

- Use reimbursement management tools or software to simplify administration

- Clearly communicate how the benefit works so employees understand how to use it

- Stay updated on IRS guidelines and healthcare regulations affecting QSEHRA

Following these practices can improve employee satisfaction while maintaining compliance.

Is QSEHRA Right for Your Small Business?

QSEHRA can be a useful option for businesses that want to support employee healthcare without the complexity of traditional insurance plans.

Employers should evaluate their workforce size, budget, and employee healthcare needs before choosing this option. Businesses that prefer predictable costs and flexible coverage options may find QSEHRA particularly beneficial.

At the same time, companies should carefully review eligibility requirements and administrative responsibilities to ensure the program fits their organization.

Conclusion

QSEHRA is a healthcare reimbursement option designed specifically to help small businesses provide health benefits in a more flexible and affordable way. Instead of purchasing a traditional group health insurance plan, employers can reimburse employees for qualified healthcare expenses and insurance premiums.

This approach allows employees to choose the health insurance plan that best fits their needs while still receiving financial support from their employer. For small businesses that want to offer healthcare benefits without high insurance costs, QSEHRA can provide a practical solution.

By understanding how QSEHRA works, who qualifies for it, and how to manage it properly, small business owners can make informed decisions about whether this type of healthcare benefit fits their organization.